Notes From the Week: Pensions, Opportunity Zones, and Looking Outside the Usual Lanes

This week’s video was inspired by Neil Bloom and his habit of stepping back to do a quick rundown of what he’s been thinking about, what he’s been seeing in the market, and where he thinks there’s room for better conversations.

So that’s what this is.

A ten-minute mental download of what’s been on my mind lately—part observation, part education, and part invitation to compare notes with people who are wrestling with similar questions.

Why I Love Managing Pensions

I genuinely love what I do.

Managing pensions puts me in front of some of the most interesting people I know—doctors, dentists, and business owners who are extremely good at what they do, who’ve worked hard to get where they are, and who are usually trying to solve very practical problems:

How do I reduce my tax burden without doing anything reckless?

How do I fund retirement without giving half of it away?

How do I create optionality for myself and my family?

One thing that continues to surprise me is how few people know what’s actually available to them, particularly on the defined benefit pension side.

Less than 5% of doctors and dentists own the real estate they practice in. Even fewer have explored the full range of retirement and tax-deduction tools that exist for high earners. And yet, once you “double-click” into these areas, entire categories of opportunity open up.

What floors me isn’t a lack of intelligence—it’s a lack of exposure.

Why Awareness Lags Behind Opportunity

Most of the professionals I work with have their basic needs met. They’re not desperate. They’re not trying to swing for the fences. And because of that, they’re understandably cautious about stepping outside their wheelhouse.

They don’t want to experiment with things their friends haven’t tried.

They don’t want to be the first one to do something unfamiliar.

They rely on trusted service providers to bring ideas to them.

That means if no one shows up with a well-reasoned, well-explained option, they simply default to what they already know—even if it’s suboptimal.

I’ve found that the biggest value I provide is education, not persuasion. Just laying out:

You can deduct a large portion of your income

You can defer taxes legally

You can design retirement contributions that actually match your stage of life

Especially for people in their 40s and 50s, this can be transformative.

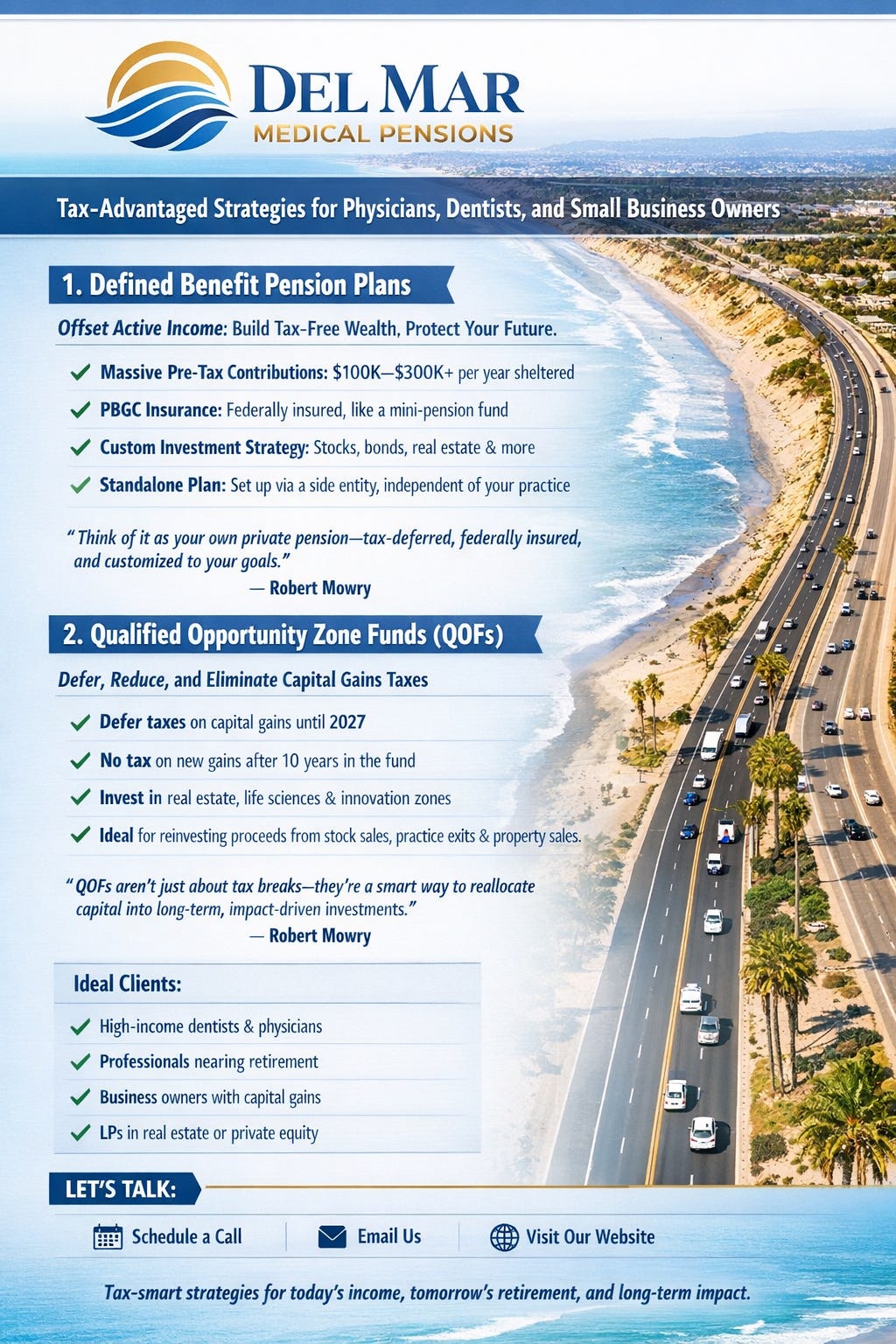

Defined Benefit Pensions: Still Hiding in Plain Sight

Defined benefit pensions are one of those tools that sound intimidating until you realize they’re built on very basic tax principles—many of the same ones multinational corporations use every day.

The idea is simple:

Convert high-tax current income into a future obligation that’s funded with pre-tax dollars.

Once people understand that, the resistance usually melts away.

I enjoy this work because I get to talk about things I find genuinely interesting—how to structure retirement intelligently, how to reclaim time, and how to give people the freedom to spend more of their lives doing what they actually want to do, whether that’s practicing medicine less or spending more time in Europe.

What’s surprising is how many brilliant people have never been walked through these concepts in plain English.

Opportunity Zones Are Back—and Supercharged

Layered on top of the pension conversations is something else that’s re-entered the picture in a meaningful way: Qualified Opportunity Zones.

Under the most recent legislation, Opportunity Zones weren’t just extended—they were meaningfully enhanced.

The core idea is powerful:

You can defer capital gains by reinvesting them into a Qualified Opportunity Fund

If you hold that investment for 10 years or more, the appreciation on that investment can be entirely tax-free

For Californians, that’s enormous.

In practical terms, you’re keeping roughly 50% more of your return than you would in a conventional taxable investment. And yet, very few people fully understand this—again, not because it’s hidden, but because it’s rarely explained clearly.

Like pensions, Opportunity Zones reward patience, structure, and proper execution.

Going Deep—But Verifying Everything

I spend a lot of time in the weeds. That’s how I’m wired.

I read the statutes. I talk to people who’ve done it before. I lean on CPAs and tax attorneys heavily. And yes, I use AI tools—extensively.

There are some impressive legal- and tax-facing AI products emerging that allow you to explore concepts far faster than waiting on email replies. That said, hallucinations are real. Verification is non-negotiable.

AI is a starting point, not an authority.

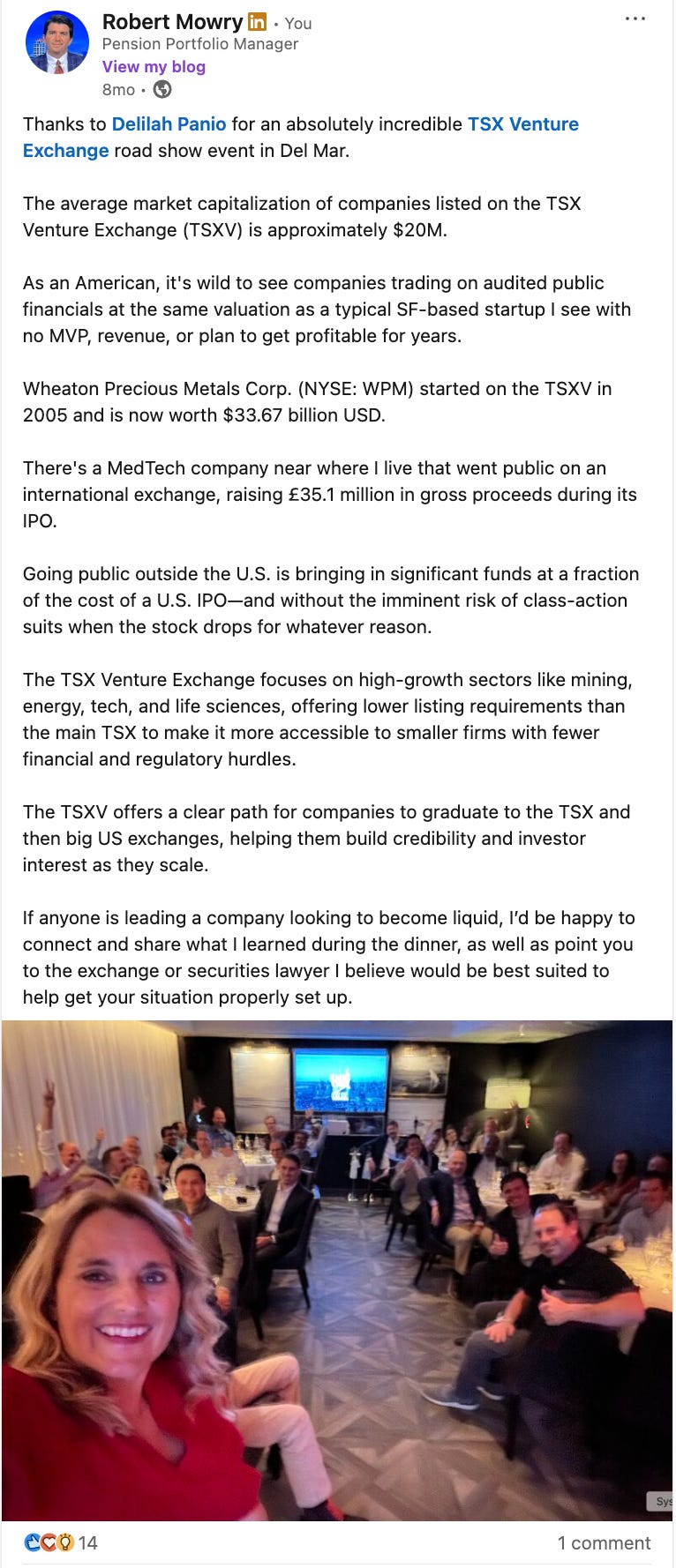

Public Markets, ERISA, and Looking Abroad

Another thread that’s been top of mind comes from the investment side of pension management.

Under ERISA, a portion of pension assets must be allocated to publicly traded securities for diversification. That constraint forces you to pay attention to markets most people ignore.

What I’ve noticed—especially recently—is the quality of companies listed outside the U.S.

There’s an impressive cohort of companies:

Listed on the Toronto Stock Exchange and TSX Venture

Listed on London’s AIM market

Based in California, including San Diego

When the Toronto Stock Exchange came to San Diego and hosted an event in Del Mar, I met founders who had:

Listed on TSX, then uplisted to AMEX or Nasdaq

Listed on Nasdaq and later accessed European markets

Used foreign exchanges to reach institutional capital they couldn’t access privately

What shocked me were the valuations.

Companies valued at $10M, $50M, $100M—levels that in California would feel like early-stage venture—yet these firms had audited financials, professional management teams, and clear paths to liquidity.

One biotech device company raised $30M publicly at a stage where they would have struggled to raise $5M privately.

That matters.

Rethinking the Exit Playbook

There’s a default assumption that the “right” exit is always:

A strategic buyer, or

Private equity

But sometimes that means your future income is just servicing the debt used to buy your own company.

In many cases, a public listing in Canada or the UK can be:

Faster

Cheaper

More liquid

More institutionally accessible

For VCs, it can mean distributing public shares, recording DPI, or selling directly into the market without waiting years for another round.

In some cases, the cost of listing is closer to the price of a car than the price of a traditional IPO.

That’s an avenue more people should at least explore.

An Open Invitation

I’ve been meeting with local firms listed on these foreign exchanges and with VCs who’ve already gone down this path successfully. The pattern is clear: there are viable alternatives that most people simply haven’t considered.

If you’re interested in pensions, Opportunity Zones, or alternative paths to liquidity, I’m always happy to talk.

And if you’re in San Francisco for JPM next week, come find me. I’ll be at side events Monday through Wednesday.

As a bit of fun: if you do find me, I’ll give you a copy of Venture Capital for Life Scientists by Will Alaynick, PhD—one of the most thoughtful, academically rigorous takes on venture capital in the life sciences I’ve read in a long time.

Education still matters. Structure matters. And thoughtful execution matters most of all.

If you want to learn more:

Subscribe to this Substack

Reach out regarding pensions

Or explore Qualified Opportunity Funds

Always happy to compare notes.

— Rob