How Dentists Can Save $50K–$100K+ Per Year in Taxes Using a Defined Benefit Plan

The savings potential from a defined benefit (DB) plan for a dentist can be substantial — here’s a breakdown of how it works and what to expect:

The Core Benefit: Massive Tax-Deductible Contributions

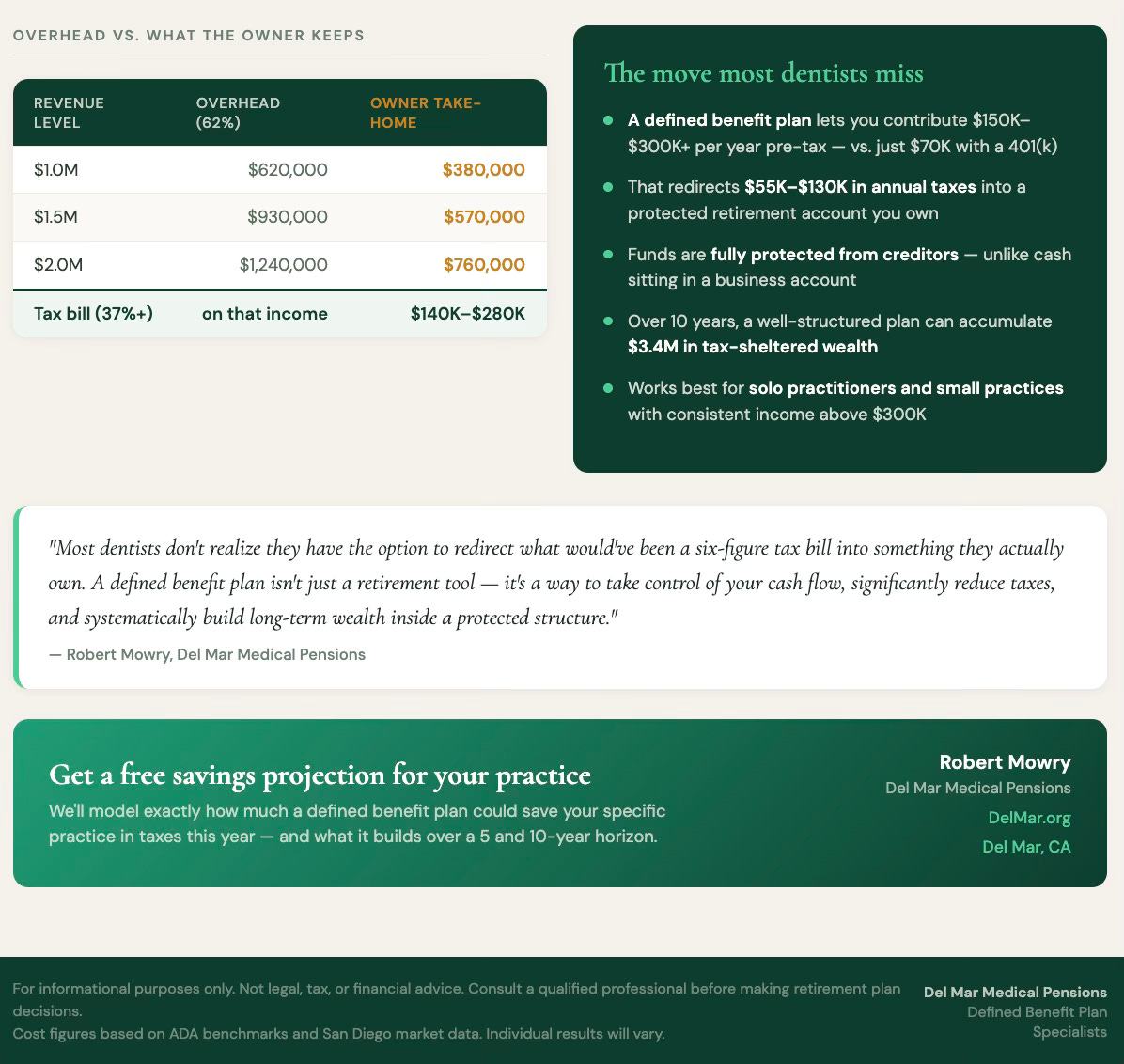

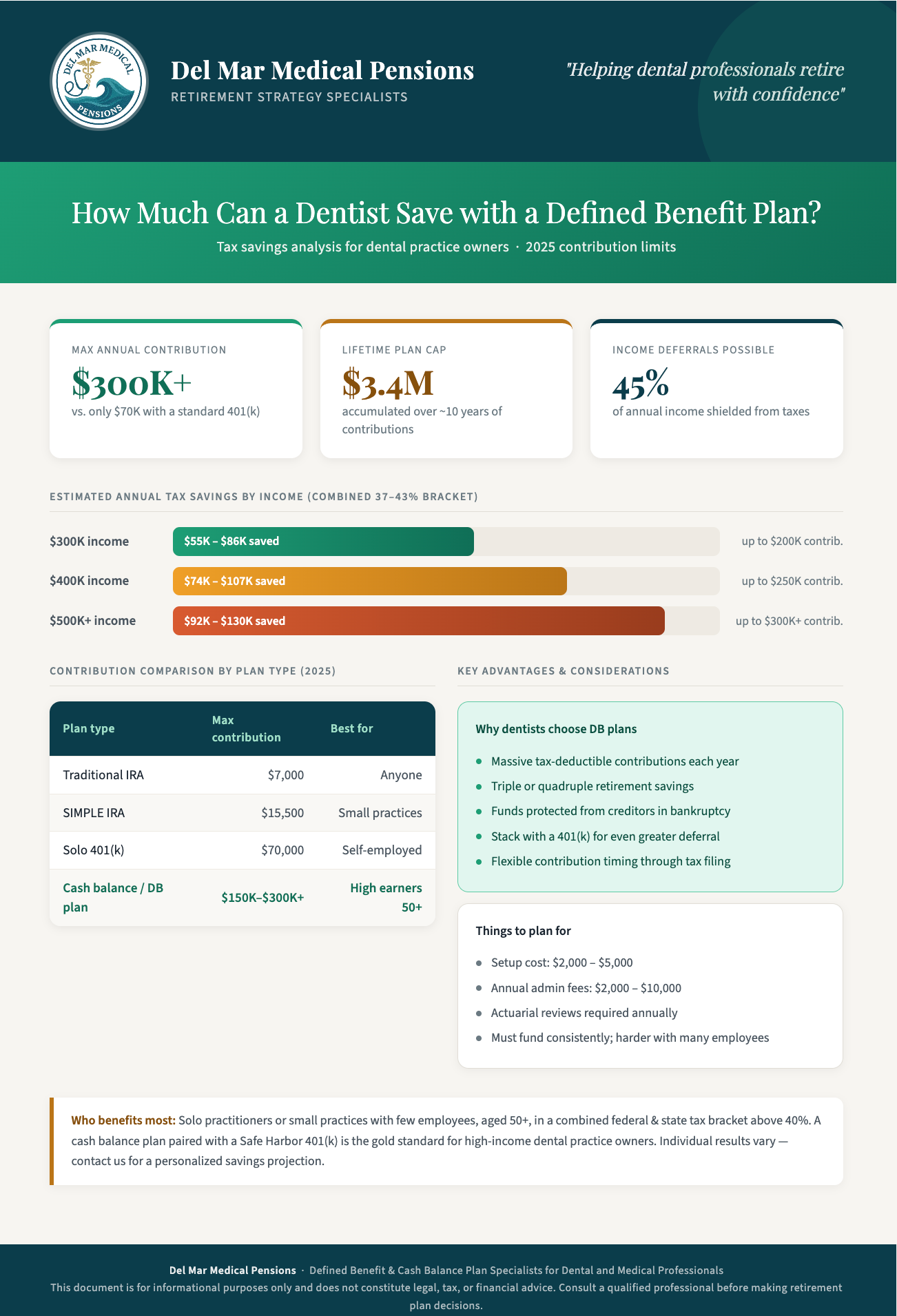

Unlike a 401(k), which caps contributions at $70,000 in 2025, a defined benefit or cash balance plan allows much higher deductions. A dentist can take a tax deduction of $150,000 per year or more, depending on their age, goals, and the structure of the plan.

The cash balance plan (the most popular DB variant for dentists) goes even further. With the potential to defer taxes on up to 45% of income, with an annual cap exceeding $300,000 depending on the beneficiary’s age, cash balance plans offer an attractive option for high-income practice owners.

Real Dollar Tax Savings

The actual tax savings depend on your bracket, but the numbers are significant:

A dentist in a combined 37% federal + state tax bracket contributing $150,000/year to a DB plan could save roughly $55,000–$60,000 in taxes per year.

For a physician or dentist earning $350,000, starting as late as age 52, a defined benefit plan can accumulate $3.4 million over 10 years.

A dentist born in 1970 may be able to make a maximum contribution of more than $215,000 annually into a cash balance plan.

Why It Works Especially Well for Dentists

The popularity of cash balance plans has surged among dentists, with over 1 in 10 such plans nationwide being utilized by dental practices. The primary advantage is enabling dental practice owners with high incomes to catch up on retirement investments with large tax-deductible deposits — particularly important given that education and practice establishment costs often delay early retirement savings.

A cash balance plan can offer the best of both worlds — dentists can potentially triple or quadruple their annual retirement savings while also receiving a tax deduction for the business.

Stacking Plans for Maximum Savings

Many dentists combine a DB/cash balance plan with a 401(k) for even greater tax sheltering. If your practice already has a 401(k) plan, combining it with a cash balance plan can unlock additional tax deferral opportunities, accelerating the growth of retirement savings.